T+1 settlement in Europe: navigating a fragmented market structure

Across global financial markets, settlement cycles are shortening. The United States moved to T+1 settlement in 2024, and Europe is preparing for the same transition on 11 October 2027. The US transition is often used as a reference point. In Europe, that comparison does not fully hold.

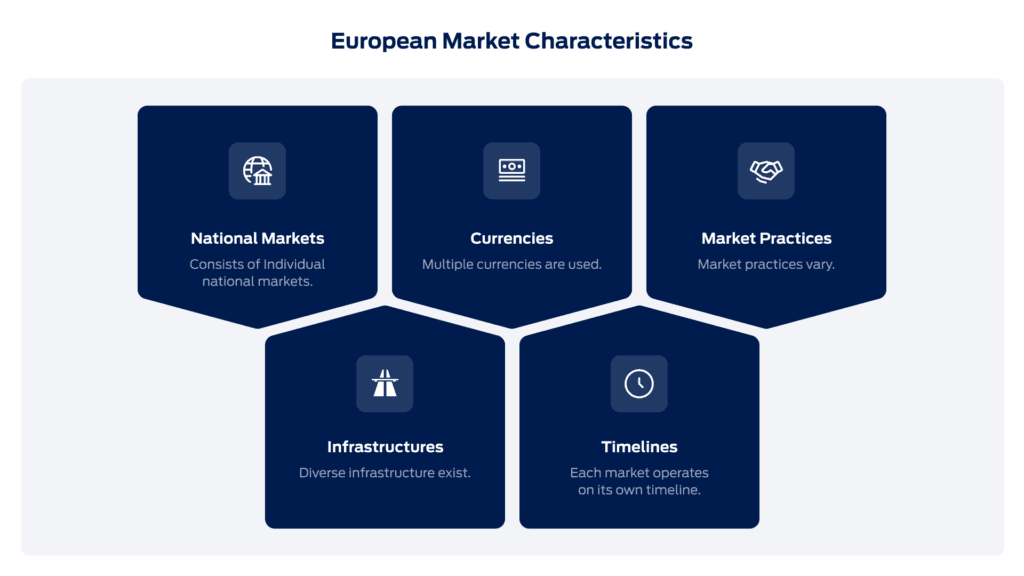

Europe does not operate as a single market, but as a combination of national markets, infrastructures, and currencies, each with its own timelines and market practices. This makes T+1 settlement in Europe fundamentally different.

Rather than a question of speed, it becomes a coordination challenge across fragmented markets, one that requires a different approach. This blog examines how this coordination challenge emerges across market structure, post-trade infrastructure, and the transaction chain.

Table of contents

One date, but not one market

T+1 settlement in Europe will take place on a single agreed date, 11 October 2027. In practice, however, this assumes a level of uniformity across European markets that does not exist.

Europe does not operate as a single market, but as a set of national markets with different trading venues, market practices, and regulatory frameworks. Many institutions operate across several of these markets simultaneously. A trade executed on a Dutch venue may involve a German asset manager, a French custodian, and settlement through an international CSD, spanning multiple market structures.

As a result, settlement depends on coordination across multiple markets, each with its own timelines and cut-offs. Under T+1, these differences are no longer absorbed within the settlement cycle, but instead directly determine whether a trade can settle on time.

Fragmented infrastructure and system dependencies

The European post-trade environment is not a single infrastructure, but a set of interconnected systems operated by different participants. Trading, clearing, and settlement are often handled separately, each with its own standards and processing logic.

This means that a single transaction depends on multiple systems rather than a single integrated infrastructure. These dependencies extend beyond securities processing. Cross-border trades require foreign exchange, funding, and cash movements to align alongside settlement, often on different timelines.

For example, a cross-border equity trade executed late in the day may require allocation, confirmation, and foreign exchange to be completed before settlement. In this case, dependencies arise between processes that operate on separate timelines. Under T+1, even a small delay can push FX execution beyond market cut-offs, forcing settlement to rely on prefunding or fail altogether. This dynamic has already been observed in markets that moved to T+1 settlement, where FX timing became a primary driver of settlement risk.

From process execution to timing alignment

Settlement is the final step in a broader operational chain. Before a transaction settles, it passes through trading, clearing, allocation, confirmation, and custody.

Shortening the settlement cycle reduces the time available for each of these steps. Activities that currently take place sequentially must occur earlier or in parallel, increasing dependencies between participants. For asset managers, this means trade allocations must be completed significantly earlier, reducing flexibility.

This shifts the focus from completing individual steps to aligning their timing. A delay in allocation affects confirmation, which in turn determines whether custodians and settlement systems can process the trade before cut-off, leaving limited scope to resolve discrepancies or exceptions.

Rather than a single process becoming faster, T+1 settlement exposes how timing dependencies determine whether a trade can settle at all.

Shifting roles across the transaction chain

The coordination challenge manifests differently across participants, as dependencies across markets, systems, and timelines shape how transactions are executed. Participants are no longer managing isolated processes, but dependencies that extend beyond their direct control.

Asset managers and pension funds face tighter timelines for allocations and confirmations, reducing flexibility and increasing their reliance on counterparties to complete processes on time.

For banks and brokers, intraday alignment becomes more complex, particularly for cross-border transactions where foreign exchange and funding need to align within narrower windows. Custodians, in turn, must manage cut-offs across multiple markets and systems, while maintaining visibility over dependencies that sit outside their direct control.

Processes for T+1 settlement therefore need to be adapted to the specific conditions of each transaction, as dependencies across the transaction chain shape execution.

Conclusion

In Europe, T+1 settlement is not simply a technical upgrade or a shorter settlement cycle, but a coordination challenge that spans market structure, infrastructure, and the transaction chain. What appears as a single change in settlement timing exposes dependencies across markets, systems, and participants that operate on different timelines.

These dependencies are not new, but become critical to settlement under T+1, directly determining whether a trade can settle, and how dependencies are managed across the transaction chain.

In this context, T+1 settlement in Europe highlights a fragmented market where coordination becomes the defining condition for successful settlement.

Want to assess your organisation’s T+1 readiness? Download the factsheet or speak with our experts.