T+1 settlement: what global markets have already learned and what Europe must address next

T+1 settlement is moving from policy debate to day-to-day delivery. In markets where it is already live, the change has proved manageable but has also made operational weak points harder to ignore. Europe now has time to prepare, but the work is practical: tighter processing windows, cleaner data, and stronger coordination across counterparties and market infrastructure.

Table of Contents

T+1 settlement in practice

T+1 settlement refers to the regulatory transition from a trade date plus two to a trade date plus one standard settlement cycle for securities transactions, requiring most trades to settle on the business day following execution.

T+1 settlement is already a daily reality in several major markets. In the United States, Canada and selected Asian markets, the shift to shorter settlement cycles has moved beyond policy discussion and into live operating practice. In Europe and the UK, the transition is targeted for October 2027, with the regulatory framework still being finalised.

Where T+1 has been implemented, the impact has been structural. Shorter settlement timelines reduce counterparty exposure and margin requirements, but they also remove much of the operational buffer that previously absorbed data inconsistencies and coordination gaps across the post-trade chain. As Europe moves closer to its transition, the question is no longer whether the industry understands the concept. It is whether European financial institutions are prepared to operate with tighter processing windows and stricter settlement discipline.

Global experience with T+1 settlement

Markets that have already adopted T+1 settlement provide a practical benchmark for Europe, showing how readiness assumptions perform under live conditions. The transition has proven workable at scale and has delivered measurable balance sheet benefits, including reductions in margin requirements and clearing fund contributions. However, it has exposed structural weaknesses that were previously concealed by longer settlement cycles.

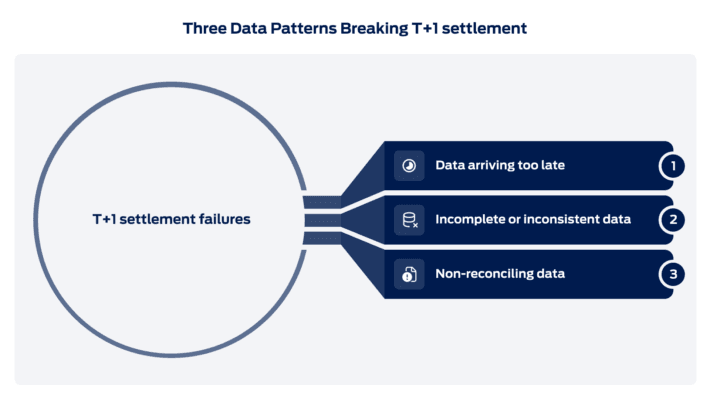

Institutions operating under T+1 report lower margin requirements and clearing fund contributions, reflecting the shorter counterparty exposure window. Faster collateral release has improved liquidity flexibility, particularly for clearing brokers, prime brokers and institutions with substantial repo or securities lending books. However, the compressed cycle demands tighter discipline across the post trade chain, as delays or data inconsistencies manageable under T+2 now quickly translate into settlement risk.

T+1 has also revealed where processes remain manual or fragmented. Late trade allocations, manual matching workflows and inconsistent settlement instructions have become persistent drivers of settlement fails. Across financial markets, one lesson has been consistently reinforced: an institution’s ability to operate under T+1 is closely linked to the readiness of its counterparties.

Why Europe’s T+1 settlement transition is structurally different

Europe approaches T+1 from a distinct starting point compared with other markets that have already transitioned. Unlike more centralised environments, European post trade processing spans multiple trading venues, numerous CSDs and ICSDs, and settlement activity conducted across several currencies within and alongside the euro area.

For European financial institutions, this dispersion translates into a broader network of cross-border dependencies across custody chains, funding arrangements and market infrastructures. Under T+1, where processing windows are compressed, delays or inconsistencies in one segment of that chain are less likely to remain contained and more likely to propagate across jurisdictions.

While many institutions operate with high levels of internal automation, the primary challenge in Europe lies less in system capability than in cross-infrastructure alignment. Differences in cut-off times, legal frameworks and settlement models increase coordination complexity and reduce tolerance for sequencing errors. In Europe, T+1 is therefore less about whether systems can process faster and more about whether market participants can operate with sufficient alignment across infrastructures and counterparties.

Operational implications for post-trade teams

At the operational level, T+1 compresses the intraday sequencing of core post trade activities. Allocation, confirmation and matching must increasingly be completed on trade date, reducing tolerance for delay across interconnected workflows.

In Europe, effective processing time is shaped not only by internal cut-off times but also by infrastructure deadlines and cross-border custody chains. Institutions with fragmented settlement models or multiple CSD connections may therefore face a disproportionate reduction in usable processing time once T+1 is implemented.

This pressure increases where activity spans multiple time zones or relies on late-day foreign exchange execution, manual allocations or end-of-day exception handling. As processing windows contract under T+1 and increase the risk of misalignment across custody and funding relationships.

Securities financing and collateral activity further increase interdependence across participants. Pre-matching discipline, timely recall processes and coordinated funding become prerequisites for maintaining settlement performance. Data integrity also becomes a real-time control issue, as static data inconsistencies or delayed instruction updates translate directly into matching breaks within the shortened cycle. Under settlement discipline regimes, operational inefficiencies carry immediate financial consequences, shifting the focus from reactive exception management to upstream control of settlement outcomes across institutional boundaries.

Europe’s roadmap to October 2027

In response, European authorities have articulated a coordinated transition plan targeting October 2027. The extended timeline reflects not only market scale but also the need to align multiple CSDs, infrastructures and jurisdictions within a single settlement framework.

The roadmap prioritises harmonised sequencing, market-wide testing and cross-border coordination, including synchronisation with the UK and Switzerland given the depth of liquidity and custody linkages across these markets. Under T+1, sequencing errors and misaligned cut-off times are more likely to transmit across custody and funding chains, making coordination and governance central to risk containment.

Europe is next, and expectations are higher

T+1 is now an established feature of major global markets, delivering measurable reductions in margin requirements and counterparty exposure while exposing weaknesses in post-trade coordination and control.

Europe represents the next structural inflection point. A dispersed market infrastructure combined with an embedded settlement discipline regime leaves limited tolerance for misalignment across custody chains, funding arrangements and counterparties. The advantage lies in hindsight: institutions can assess their preparedness against observed outcomes rather than theoretical assumptions.

As October 2027 approaches, differentiation will depend less on formal readiness and more on demonstrable operating model coherence. In a settlement environment defined by compressed timelines and stricter fail consequences, preparedness will be reflected in sustained settlement performance rather than declared intent.

If you would like to explore the implications of T+1 for your organisation, please don’t hesitate to contact us or download our factsheet.